By Bob Iaccino

At a Glance

- Gold’s performance can vary significantly depending on economic, geopolitical and market factors

- Historically, gold performs well when interest rates are falling as investors seek safe-haven assets

Gold has long been considered a safe-haven asset, with investors turning to the precious metal during economic uncertainty. However, its performance can vary significantly depending on the prevailing economic conditions. With the Fed’s next action likely to be interest rate cuts, how has gold historically performed under different combinations of falling or stable interest rates, economic growth and inflation?

1. Falling Interest Rates, Slower Economy, and Falling Inflation (Soft-Landing)

Gold has often performed modestly during periods characterized by falling interest rates, a slower economy and falling inflation. A prime example occurred in the early 2000s, particularly from 2001 to 2003.

The U.S. economy slowed significantly after the dot-com bubble burst and the 9/11 attacks. The Federal Reserve responded by cutting interest rates aggressively, from 6.5% in January 2001 to 1% by June 2003. Inflation declined during this period, falling from 3.4% in 2000 to 1.6% in 2002.

Gold’s performance during this time was generally positive, though not spectacular. The price of gold rose from around $270 per ounce in early 2001 to about $350 per ounce by the end of 2003, representing a gain of approximately 30% over three years.

The relatively modest performance of gold during this period can be attributed to several factors. While lower interest rates typically support gold prices by reducing the opportunity cost of holding the non-yielding asset, the deflationary environment and slower economic growth created conflicting pressures.

Looking to the Fed’s September decision and beyond, a hybrid scenario where inflation is controlled without triggering a recession – involving gradual rate cuts and stable growth – could still support gold prices through a mix of inflation concerns and accommodative policy. This could potentially make gold an effective hedge in the coming months.

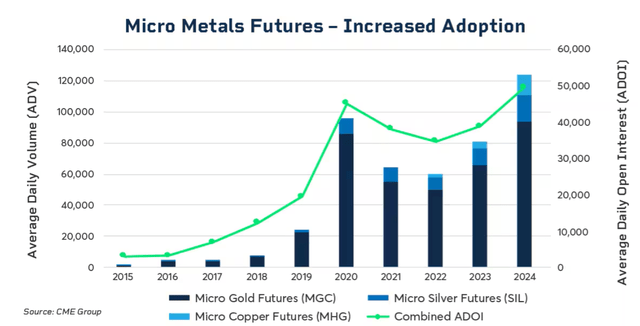

As of the end of Q2 2024, Micro Gold futures were already trading 27% more YTD at 93K contracts per day on average, predominantly from price volatility in the market. The most recent data from August shows Micro Gold futures ADV increased 170% compared to August 2023 to 124,000 contracts.

2. Rapidly Falling Interest Rates, Rapidly Slowing Economy, and Falling Inflation

Periods of rapidly falling interest rates, a quickly decelerating economy and falling inflation have typically been positive for gold as investors seek safe-haven assets. A prime example occurred during the 2008 Global Financial Crisis.

In response to the crisis, the Federal Reserve slashed interest rates from 5.25% in September 2007 to effectively zero by December 2008. The U.S. economy contracted sharply, with real GDP falling by 2.5% in 2009. Inflation also declined, dropping from 3.8% in 2008 to -0.4% in 2009.

Gold performed exceptionally well during this period of economic turmoil. The price of gold rose from around $700 per ounce in late 2007 to over $1,000 per ounce by early 2009, and it continued to climb in the following years, reaching a peak of nearly $1,900 per ounce in 2011.

Gold’s strong performance during this crisis can be attributed to its status as a safe-haven asset. As the financial system teetered on the brink of collapse and traditional assets like stocks and real estate plummeted in value, investors sought the perceived safety of gold. While the economy remains relatively stable as of early September, any signs of a more severe downturn could prompt more aggressive Fed action and emphasize gold’s role as a safe haven.

3. Falling Interest Rates, Stable Economy, and Rising Inflation

The period from 2003 to 2006 provides another interesting case study. The U.S. economy was relatively stable during this time, with GDP growth averaging around 3% annually. Inflation rose moderately, increasing from 1.6% in 2002 to 3.2% by 2006. The Federal Reserve, which had kept interest rates low in the early 2000s, began a gradual tightening cycle in 2004 but maintained a generally accommodative stance.

Gold prices performed strongly during this period, rising from about $350 per ounce in early 2003 to over $700 per ounce by mid-2006, representing a gain of approximately 100% in just over three years.

The positive performance of gold during this time can be attributed to a combination of factors. Rising inflation created a demand for gold as an inflation hedge, and since interest rates were only increased gradually, the opportunity cost of holding gold remained relatively low. As of early September, the Fed is signaling potential rate cuts while inflation remains above target. This environment could benefit gold, echoing the 2003-2006 period.

Patterns Aren’t Predictive

The historical examples demonstrate that gold’s performance as an asset can vary significantly depending on the prevailing economic conditions. However, some general patterns emerge:

- Gold tends to perform well during periods of economic uncertainty, mainly when interest rates are falling and investors seek safe-haven assets.

- Rising inflation, especially when combined with low or falling interest rates, creates a particularly favorable environment for gold prices.

- In deflationary environments, gold’s performance may be more muted, but it can still attract investors seeking a store of value during economic downturns.

- Stable economic growth can provide a supportive backdrop for gold investment, particularly when combined with accommodative monetary policy and rising inflation expectations.

It’s important to note that while these historical patterns can provide insights, the gold market is influenced by a complex interplay of economic, geopolitical, and market factors, and its behavior can sometimes deviate from historical norms. As the Fed continues to assess and adjust U.S. monetary policy, gold will be an area to monitor for many market participants.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here