On 08/08/2024, Royalty Pharma plc (NASDAQ:RPRX) presented its Q2 earnings. Following a solid Q1, the company raised its 2024 outlook, with Portfolio Receipts expected to achieve $2.7/2.75 billion results. We positively view this announcement; however, today, we decided to focus on an ongoing downside.

Downside Protection

In our initiation of coverage, we reported how the Vertex franchise is one of the most significant portfolio receipt contributors. In detail, we explained:

The cystic fibrosis franchise is based on four therapies and accounts for 33% of RP’s adjusted cash receipts. In 2022, the franchise generated $811 million of royalties for RP (25% of its total). This drug was approved in October 2019 and is expected to create a royalty revenue stream by 2037, when the patent expires. Despite that, Vertex is moving on with another application already in phase 3. If approved, this could significantly limit RP’s earnings.

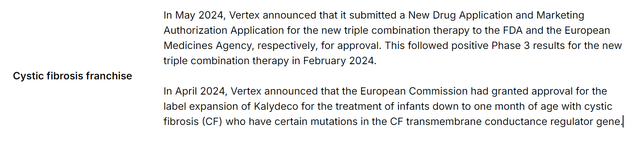

At that time, Royalty Pharma’s CEO described the patent position as “defensible and solid.” In Q2 2024, Vertex was granted approval in the EU following a positive read-out from the FDA (Fig 1). After the just-released Q2 report, the company’s top royalty contributor remains the Cystic Fibrosis franchise, with approximately 32% of top-line sales. In number, the franchise reported $195 million in sales in Q2. Therefore, we might expect lower royalty when the new Vertex goes online. Given Royalty Pharma’s balance sheet and earnings diversification, these risks still appear manageable. What we do not like is the lack of clarity during this period.

Vertex Update

Source: RP press release – Fig 1

Q2 Earnings Results

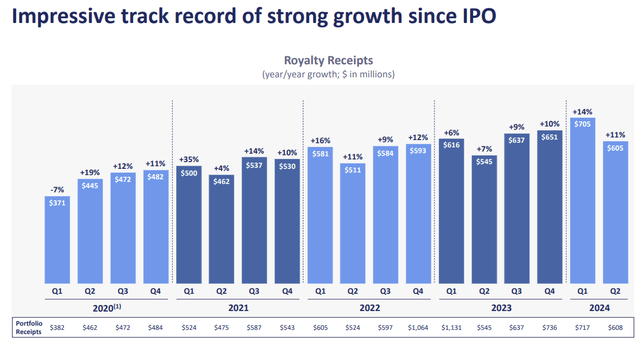

The company’s royalties increased by 11% to $605 million (Fig 2). This has happened twelve times out of 18 quarters since its IPO four years ago. The product portfolio receipts were driven by the solid performance of Evrysdi, Tremfya, and Trelegy, which were up by 91%, 34%, and 32%, respectively. In absolute value, we should also report the strong results of the Cystic Fibrosis franchise, which is the company’s main downside risk. Going down to the P&L analysis, the company’s Q2 adj. EBITDA reached $560 million. RP’s operational costs are minimal, and we report a new Head of Resources. This supports the company’s operating leverage. On the other hand, high operating leverage also carries the risk of substantial losses if top-line sales decline. This is why it is critical to understand Vertex franchise development better.

RP results

Source: RP Q2 results presentation – Fig 2

Our Positive View

- The company (once again) increased its yearly guidance, and this solid set of results cannot go unnoticed.

-

Secondly, we continue to view the company’s capital deployment as underappreciated.

-

The company indicated a close look at obesity and autoimmune disease. With the right opportunity, they would be willing to raise additional debt to 4x leverage. This, again, might offer a positive catalyst to drive investor interest/sentiment.

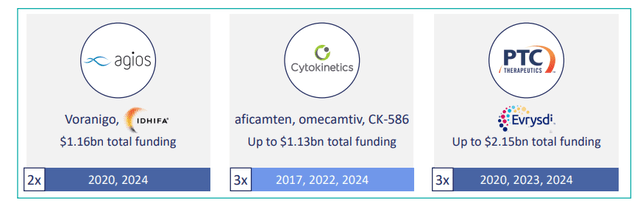

At June’s end, the company reported new transactions for almost $2 billion. That said, RP has ample liquidity to finance new royalties acquisitions (and diversified its earnings from the Cystic Fibrosis franchise). Therefore, it is vital to report our view on the latest three deals (Fig 3).

- Here at the Lab, we believe Vorasidenib royalty will significantly contribute over time. The company reported a new acquisition for approximately $900 million, entitling Royalty Pharma to a 15% royalty on USA net turnover < $1 billion and a 12% royalty on net turnover > $1 billion. The drug has the potential to be the first targeted therapy in IDH-mutant glioma, offering an alternative to chemotherapy. This results in lower toxicity for patients. The company anticipates $1 billion in peak annual sales, so we estimate a double-digit IRR through 2038. In addition, as a downside protection, this therapy is not included in the IRA;

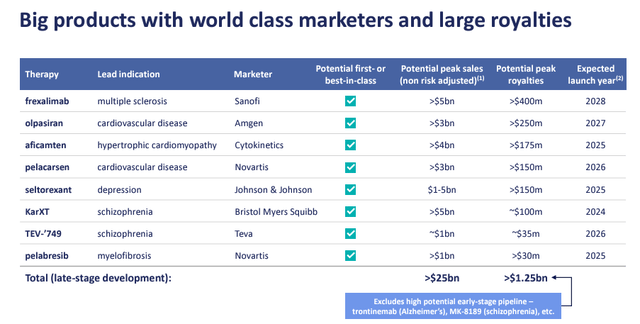

- The company also recently announced a deal with Cytokinetics (CYTK). This is a follow-up $575 million investment and supports Aficamten commercialization. RP is entitled to a 4.5% royalty on annual net turnover < $5 billion and a 1% royalty on turnover > $5 billion. Based on the estimates, our team expects a multi-billion dollar peak sales, which might further enhance the company’s value (Fig 4);

- Lastly, the company increased its royalties on Roche’s (OTCQX:RHHBY, OTCQX:RHHBF, OTCPK:RHHVF) Evrysdi, which is already in the RP product portfolio. In the next twelve months, this should deliver a Portfolio Receipts result of $100 million.

RP new investments

Fig 3

New key royalties

Fig 4

Adjusting Estimates and Valuation

Following the recent investment, our year-end net debt projection has changed. We now forecast net debt from $5 billion to $6 billion. This includes a higher FCF generation supported by the current portfolio, and is also based on the Vorasidenib deal and the initial payment of $250 million for Cytokinetics. The RP press release reported that the Vorasidenib payment is subject to FDA approval. Following the company’s guidance and the latest update on the royalties’ annual sales, we also increase our portfolio receipts estimates from $2.65 billion to $2.7 billion. This is based on the Evrysdi uplift top-line sales (while Cytokinetics and Vorasidenib royalties will start contributing after the regulatory approvals). Even if this appears to be a small change, this company has an EBITDA margin of 93%. We should remind you that the company’s operating & professional costs are minimal, and there is no D&A. In our estimates, we increased our EBITDA projection to $2.49 billion and net earnings to $2.32 billion. Therefore, we arrive at a 2024 EPS of $3.91.

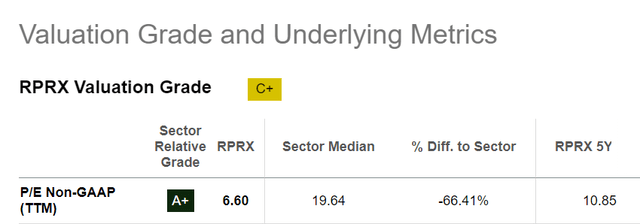

At the time of writing, the company trades at a P/E below 7x and an EV/EBITDA of 8.6x. In our initiation of coverage, we reported how other royalty companies in oil and gold usually trade at a premium valuation compared to their respective commodity peers. This is not the case with RP. Indeed, Sanofi (SNY, OTCPK:SNYNF, GCVRZ), Roche, and Novartis (NVS, OTCPK:NVSEF) trade at a P/E above 14x on average in our Pharmaceutical coverage. Therefore, we continue to see RP’s valuation as highly compelling. For consistency reasons, continuing to value the company with a target P/E of 10x, aligned with its last five years’ average (Fig 5), we reach a target price of $39.1. This implied a discount to pharma peers above 40% and a potential share re-rating ahead.

SA Valuation Data

Fig 5

Risks

Taking advantage of our previous coverage risks section (Fig 6), we also report the following potential negative downside: RP’s unique business model makes it the only US-listed public player of its kind. Therefore, it is hard to justify a valuation (or a peer group analysis). Another risk is the worse-than-expected performance of current investments or new royalties with lower-than-expected IRR. The company has several assets in late-stage development, including:

- Pelacarsen and Olpasiran for cardiovascular disease;

- Aficamten for hypertrophic cardiomyopathy,

- KarXT for schizophrenia

- Frexalimab for multiple sclerosis.

Having said that, KarXT from AbbVie (ABBV, ABBV:CA) faces a competitive risk, with pivotal data expected in Q4 2024. In addition, comp from Frexalimab might create additional uncertainty.

Mare Ev. Lab previous risks section

Fig 6

Conclusion

The company’s share price reflects little to no value from future investments. We recognize the cystic fibrosis royalty loss and believe this is fully priced into shares. While sell-side analysts continue to perceive the higher for longer interest rate environment as a headwind, the company is progressing well due to its low refining cost and ongoing difficulty funding environment in the biotech sector. This is why we confirm our buy rating.

Read the full article here