Qudian Inc. (NYSE:QD) defines itself as a “consumer-oriented technology company. The company historically focused on providing credit solutions to consumers. Qudian is exploring innovative logistics services to satisfy consumers’ demand for e-commerce transactions by leveraging its technology capabilities.”

In the latest Fourth Quarter and Full Year 2023 report, Mr. Min Luo, founder and CEO, also added:

Looking ahead, we are enthusiastic about unveiling our strategic initiative to venture into new online and offline retail business that bridges Chinese supply chain advancements with discerning global consumers, complemented by a “Buy Now, Pay Later” solution. Detailed insights into these endeavors will be communicated in due course.

Now, do you have an idea what kind of business Qudian is? No? I had the same problem. Let us therefore look at the history of Qudian’s business, as this will bring us more clarity as to what kind of business it is.

Business Overview

In 2019, Qudian provided small online consumer credits through their mobile app in China and targeted young individuals who needed credit for their discretionary spending. They used a big-data-driven AI model to assess credit risk. Later, in 2020, Chinese regulators intensified a crackdown on small P2P lenders, so the existing business model has no more perspective. Therefore, the company decided to leave the credit business, which was completely halted by the end of 2022.

They also offered budget auto financing products under the Dabai Auto brand, but the business was not successful and was shut down in 2019.

Qudian quickly reinvented itself in 2020 and launched the e-commerce platform Walimu, which offered online luxury fashion products. However, it was not a success, and the company was shut down.

In 2021, Qudian launched Wanlimu Kids Clubs, offering “early childhood education,” whatever that may mean, but again, the business was not successful and wound down in November 2022.

But the management did not give up, and in March 2022, they started “QD Food,” which was making and selling “ready-to-eat” dishes. CEO Luo Min spent approximately $30 million on live stream promotion of the business. As you can probably guess, this business was also not a success, and the company recorded a loss of RMB 361 million ($50 million) in 2022.

If you would like more information about CEO Min Luo, his business story, and how he tried to promote QD Food, I recommend that you read this article.

As the food business turned out to be another disaster, in December 2022, the company reinvented itself as a smart last-mile delivery business. They operate under the name “Fast Horse Express” in the US, Canada, Australia, and New Zealand. The last-mile delivery business is tough, as they have to compete with big players like FedEx, United States Postal Service, UPS, DHL, and others. However, they have a unique approach. They work on an individual contractor model and allow you to schedule your working hours so you can deliver parcels in your spare time. All you need is your own car and 15 minutes of online training, and you are ready to go.

If you think that this business was also a disaster, you are right. The “Fast Horse Express” service has 1,268 reviews on the Product Review page, with 93% of them being negative and a rating of 1.3 stars out of 5 (five being the best). Not the kind of business you would like to own. Just look at the graph below; the operating expenses were much higher than revenues.

Qudian 2023 quarterly results in US millions (Author)

Based on the current performance of “Fast Horse Express,” I anticipate that this business will also wind down. This is supported by the statement of the CEO, who mentioned that they intend to “venture into a new online and offline retail business that bridges Chinese supply chain advancements with discerning global consumers, complemented by a “Buy Now, Pay Later” solution.”

Will this new business be successful? I have no idea. However, based on the current track record, Qudian is a story of failure.

To assess the magnitude of this failure, we need to examine the financial reports.

Business Financials

Last year, the financial performance of the company was dismal. Take a look at the figures for yourself.

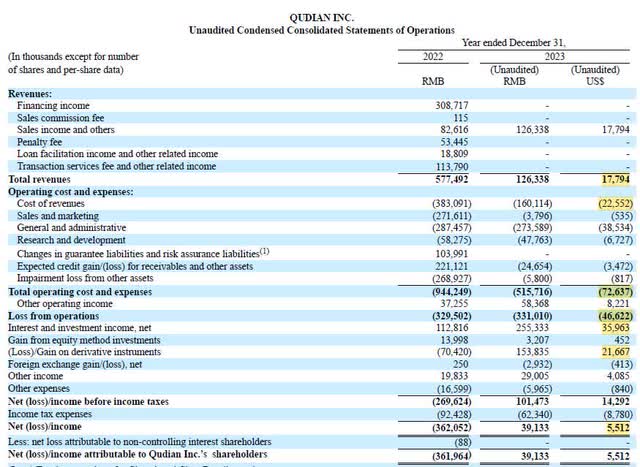

Qudian Fourth Quarter and Full Year 2023 Report

They spent $22.5 million to generate $17.8 million in revenue. Add $38.5 million for general and administrative expenses (including $10.7 million spent in Q4 for third-party professional services and travel expenses), $6.7 million for research and development as they explore new opportunities, and various other expenses, and you arrive at $72.6 million in total operating expenses. To spend such a large sum of money and only generate $17.8 million in revenue requires talent.

The bottom line was salvaged by the interest income from bank deposits and derivate investments, which are speculative and may yield positive or negative returns, as seen in 2022.

Looking at the income statement, I have a feeling that it would be better to stop all operations, minimize the costs, and invest the existing cash ($1.1 billion) in US Treasury bills to earn a 5.2% interest rate. This would yield $57.2 million annually. However, anyone can do this without incurring millions in operating expenses.

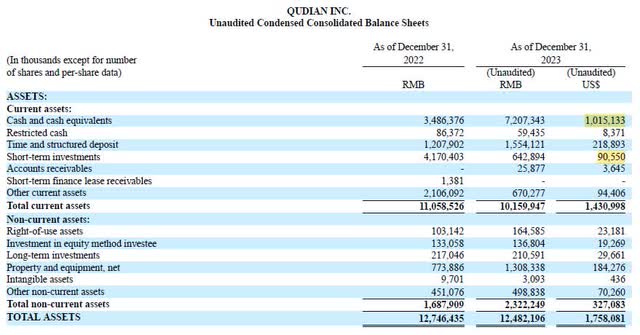

The cash on the balance sheet primarily stems from funds raised during the IPO on the NYSE in 2017, where they raised $900 million. Initially, the cash was utilized for business purposes, with assets mainly in the form of receivables. However, as the company’s business activities dwindled and they exited the loan business, the assets reverted to cash. The positive aspect is that stockholders’ equity stands at $1.646 billion, which is $200 million higher than in 2017, indicating no ongoing value destruction. However, accessing this money is currently challenging.

Qudian Assets (Qudian Fourth Quarter and Full Year 2023 Report)

There is approximately $1.1 billion in cash and $600 million in other assets. Assuming that $200 million of these assets can be converted to cash during the company’s liquidation, we have a total of $1.3 billion. Then we have to deduct liabilities, which amount to only $111.9 million, so we get net cash of $1.2 billion, with 204 million shares outstanding. This gives me a value of $5.88 per share trapped in the company.

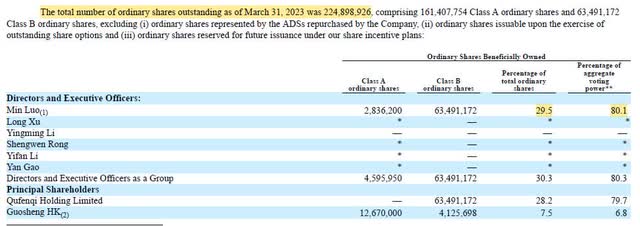

The question is, how can shareholders access this $5.88? The answer is that unless the CEO decides to liquidate the company and distribute the assets to shareholders, they will not receive this money. This is because the CEO owns more than 29.5% of all shares (2.8 million were acquired through his spouse in 2023) and controls 80.1% of the voting power.

Qudian share ownership (Qudian FY2022 Report)

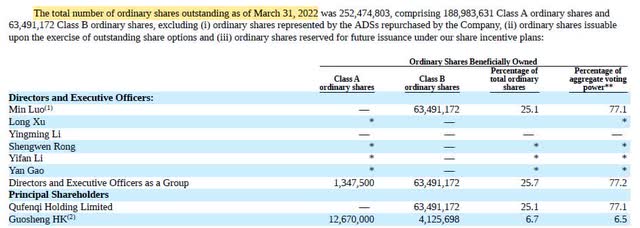

For comparison, below is the share ownership in March 2022.

Qudian share ownership (Qudian FY2021 Report)

As you can see, the CEO increased his ownership of the company by 4.4% in one year through indirect share ownership and with the help of share buybacks.

When we examine the last Fourth Quarter and Full Year 2023 report, we find two interesting statements regarding the share buyback program:

In the past 12 months ended March 13, the Company has in aggregate purchased 34.7 million ADSs in the open market.

…our Board has approved a new share repurchase program in March 2024 to purchase up to US$300 million worth of Class A ordinary shares or ADSs in the next 36 months starting from June 13, 2024.

This indicates to me that the CEO is attempting to acquire a larger stake in the business, thereby owning more of the cash on the balance sheet. I would not be surprised if the CEO’s share ownership by the end of March 2024 exceeds 33%.

What to do with Qudian stock?

From a long-term perspective, I believe this stock is a sell due to the company’s continual reinvention into new businesses. It’s unclear what exactly you’re investing in. Is it a last-mile delivery company, a food business, or a “Buy Now, Pay Later” business? And what will it become next year? Without clarity on the company’s future revenue sources, it’s challenging to estimate its long-term financial prospects.

However, from a short-term perspective, I would put Qudian on hold because of the announced $300 million buyback program scheduled to start in June of this year. With $300 million allocated to repurchasing shares of a company with a market cap of $562 million, the stock price should increase.

But will the stock price ever reach the level of cash per share held on the balance sheet? I doubt it, unless the company establishes a profitable business model that consistently generates positive free cash flow. If this were to occur, I would reconsider my stance on whether to buy this stock.

Conclusion

Qudian is a company that is constantly trying to find itself and reinvent itself, almost every year. So far, the search has not been successful, but the CEO is not giving up. In my view, the best outcome for the shareholders would be if the CEO, Luo Min, liquidated the company, sold all assets, and paid the available cash to shareholders so they could decide how to invest it again. Under this scenario, each shareholder would receive approximately $5.88 per share, which is not bad as the current stock price is $2.50 per share. However, I do not think that this is a realistic outcome as the CEO holds more than 80% of voting power and he is desperately trying to start some business, which would be finally successful.

In my opinion, Qudian is not a stock to invest in because the future of the company is uncertain and the business model is changing almost each year. For me, it is, from a long-term perspective, a sell. In the short term, the stock is a hold, as I expect that the stock price will go up based on the fact that the company will spend $300 million on share buybacks. How much will the stock go up? It is impossible to predict. Ultimately, it is up to each shareholder to decide whether to participate in the share buyback game or sell now and invest in a more promising opportunity.

Read the full article here