Investment Thesis

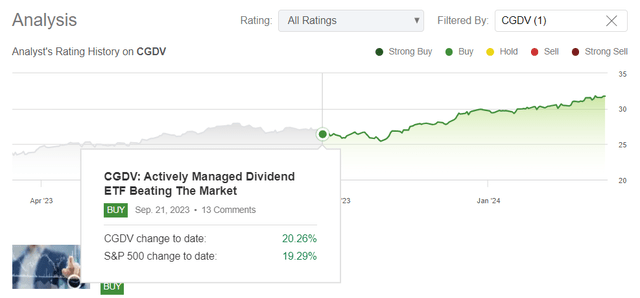

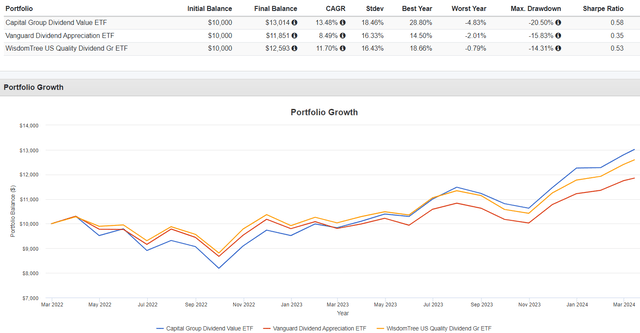

Six months ago, I initiated coverage of the Capital Group Dividend Value ETF (NYSEARCA:CGDV), listing impressive performance, a unique multi-manager structure, and solid fundamentals as reasons for my “buy” rating. Since then, it’s slightly outpaced the S&P 500 Index, one of only a handful of large-cap value ETFs to do so over this period.

Seeking Alpha

As an actively managed fund, CGDV managers can trade stocks as they see fit. However, over the last six months, they’ve only slightly changed the portfolio and kept estimated earnings growth high, ensuring continued participation in this rising market. It’s a nice feature, but perhaps even better is how well CGDV can complement S&P 500 Index funds. Along with a detailed fundamental analysis comparing CGDV with the Vanguard Dividend Appreciation ETF (VIG) and the WisdomTree U.S. Quality Dividend Growth ETF (DGRW), this article includes a fund overlap by weight analysis that suggests adding CGDV is an efficient move. I look forward to taking you through this in greater detail below and explaining my decision to reiterate my “buy” rating on this exciting dividend ETF.

CGDV Overview

Strategy Discussion

According to its fund page, one of CGDV’s main objectives is to “produce consistent income that exceeds the average yield of the S&P 500 by focusing on companies that pay dividends or have the potential to pay dividends.” The ETF is managed by five portfolio managers who follow “The Capital System,” which “combines independent high-conviction decision-making with the diversity that comes from multiple perspectives.” In my prior review, I profiled the five managers and determined there was minimal overlap in managers’ respective areas of expertise. As a refresher, here are some brief backgrounds:

1. Christopher Buchbinder: telecommunication services, auto manufacturers, auto parts, and equipment.

2. Martin Jacobs: industrial machinery and electrical equipment.

3. James Lovelace: beverages, tobacco, restaurants, and household and personal products.

4. Keiko McKibben: aerospace and defense, information technology, industrial machinery, and business services.

5. James Terrile: health care supplies, medical equipment, biotechnology, and pharmaceuticals.

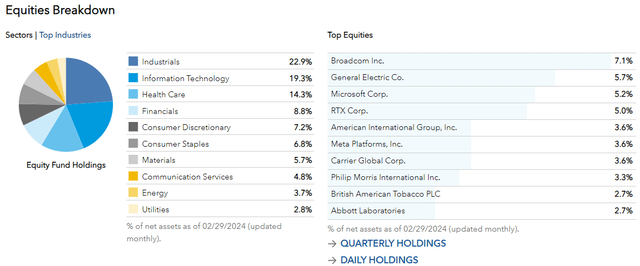

Each manager selects stocks from their respective areas of expertise, but notably, The Capital Group does not highlight energy, financials, materials, real estate, or utilities. These five sectors are underrepresented in the fund, totaling just 21% of the current portfolio on February 29, 2024.

The Capital Group

Broadcom (AVGO) is the top holding, but CGDV overweights the Industrials sector at 22.9%, perhaps due to the expertise of portfolio managers Jacobs and McKibben. Top stocks in this sector include General Electric (GE), RTX Corp. (RTX), and Carrier Global (CARR). However, the Industrials sector is relatively low-yielding. CGDV’s selections yield only 1.45%, while Consumer Staples yield the most at 6.82%.

Dividend Analysis

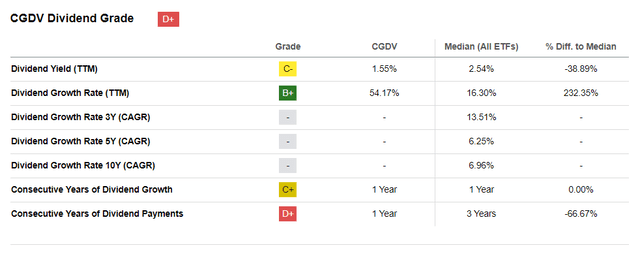

Beating the S&P 500 Index on dividend yield isn’t challenging. The SPDR S&P 500 ETF (SPY) yields 1.29%, and approximately 90% of large-cap value funds have yields above this figure. CGDV’s 1.55% trailing yield isn’t much better, and Seeking Alpha has assigned it a poor “D+” overall Dividend Grade.

Seeking Alpha

CGDV is a relatively new ETF, having only launched on February 22, 2022, so it has yet to have the opportunity to build up any dividend growth history. However, based on its current selections, mid-to-high-single-digit dividend growth is probable over the long run. Its constituents have weighted average three- and five-year dividend growth rates of 10.97% and 6.24%, respectively, and the current Index yield is 2.14%. After deducting CGDV’s 0.33% expense ratio, 1.81% is the net yield, which is about the same as DGRW and VIG.

CGDV Fundamental Analysis

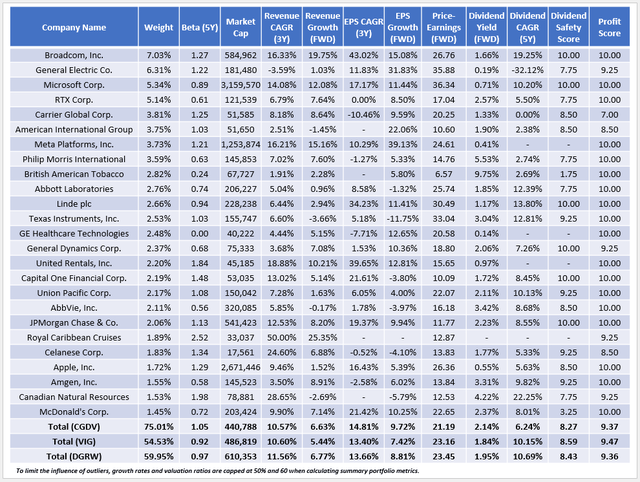

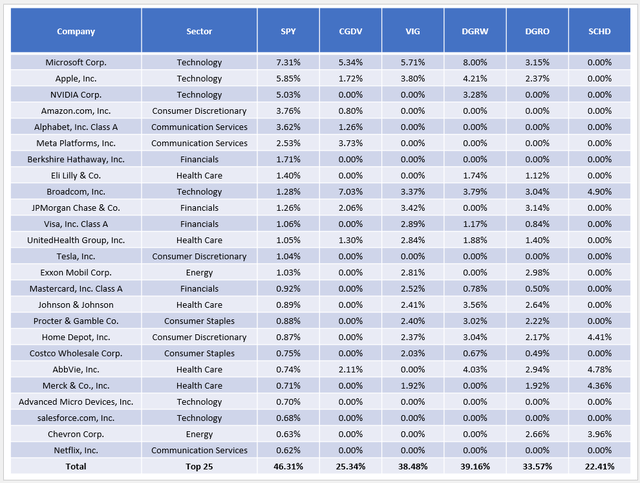

The following table highlights selected fundamental metrics for CGDV’s top 25 holdings, totaling 75.01% of the portfolio. Please note these are cash-adjusted weights as of March 14, 2024, as CGDV has a 3.52% position in the Capital Group Central Cash Fund (CMQXX).

The Sunday Investor

Here are four takeaways:

1. CGDV holds 50 stocks, so it’s a very focused portfolio compared to VIG and DGRW, which hold 311 and 296. It also has 92.15% allocated to its top 25 sub-industries compared to 75.54% and 82.36% for VIG and DGRW, so it may not make the best core holding in your portfolio. However, it could complement several ETFs quite well, and “fit” is something I will evaluate shortly by comparing overlap with VIG, DGRW, the iShares Core Dividend Growth ETF (DGRO), the Schwab U.S. Dividend Equity ETF (SCHD), and the Vanguard High Dividend Yield ETF (VYM).

2. CGDV has a 1.05 five-year beta, which is high for a large-cap value ETF. The category average is 0.97, and funds with betas above one tend to be deep-value funds with virtually no earnings growth. Examples of such funds you might be familiar with include the Pacer US Cash Cows ETF (COWZ), the Invesco S&P 500 Enhanced Value ETF (SPVU), and the newly-launched VictoryShares Free Cash Flow ETF (VFLO), but CGDV is different. While it is slightly more volatile than most peers, its 9.72% estimated earnings growth rate is excellent for the category, ranking #4/97. This high ranking is why CGDV has performed so well in this growth-favored market, outpacing VIG and DGRW by 4.99% and 1.78% per year since February 2022.

Portfolio Visualizer

3. The downside is that CGDV trades at 21.19x forward earnings, or #86/97, in the large-cap value category. With relatively high valuation ratios and beta, it would not be surprising if CGDV underperformed in a market drawdown. The graph above shows that it declined by 20.50% between April and September 2022, which matched the drawdown for SPY.

Portfolio Visualizer

4. CGDV selects high-quality stocks, evidenced by the portfolio’s 9.37/10 profit score, which I calculated using Seeking Alpha Factor Grades. However, CGDV’s weighted average free cash flow margins are only 13.02%, which ranks #47/97. It could limit future dividend growth, and as we can see in the fundamental analysis table, CGDV’s constituents have lower five-year dividend growth rates and a lower dividend safety score than VIG and DGRW. Therefore, it’s probably not optimal for DGI investors. Instead, the main goal is capital appreciation with slightly more yield than SPY.

How Well Does CGDV Complement Other ETFs?

Though CGDV is actively managed, I expect its holdings to stay mostly consistent, given how its managers operate with high conviction. In contrast, passive ETFs like SCHD must change their holdings at each scheduled reconstitution. For example, I expect SCHD to drop Broadcom, a top-performing stock over the last year, on Monday. This deletion would boost SCHD’s yield but could decrease future dividend growth and total returns, and that change is likely to draw mixed reviews. CGDV isn’t bound by such a schedule, which could be an advantage, depending on your goals.

While we can’t control what other ETFs do, CGDV seems like a solid complement to broad-market funds. The table below highlights each ETF’s allocations compared to SPY’s top 25 holdings.

The Sunday Investor

Notice how CGDV has far less allocated (25.34%) to SPY’s top 25 holdings than VIG and DGRW. CGDV has a 35.15% overlap by weight in total with SPY compared to 44.77% and 49.08% for VIG and DGRW, so it is a better complement. SCHD is the most different, but the caveat is that it lacks a significant earnings growth component, currently estimated at just 0.94% over the next year. CGDV’s 9.72% growth rate means it’s far more likely to outperform in bull markets.

Investment Recommendation

CGDV is one of only a handful of large-cap value ETFs with a high estimated earnings growth rate. This feature is why it’s outperformed most peers since its February 2022 launch, but I caution readers that it’s slightly risky for the category. CGDV has an above-average 1.05 five-year beta, a forward P/E that ranks in the bottom decile, and a short drawdown history that’s only as good as SPY. Its 1.81% expected dividend yield is also not competitive with most dividend ETFs, but with earnings growth rates declining across the board, I appreciate that CGDV’s fund managers aren’t just picking the most beaten-down stocks for their high yields. Managers emphasize the quality and growth factors, and that’s comforting for long-term investors.

CGDV’s growth and valuation combination is better than VIG and DGRW’s. It also serves as a better complement to SPY based on my holdings analysis. Investors should weigh this against CGDV’s weak diversification at the company and sub-industry levels and remember that it’s easier to construct a fundamentally strong portfolio with fewer holdings. Nevertheless, CGDV is a well-constructed ETF that I think pairs well with broad-market ETFs like SPY, and as such, I’ve decided to reiterate my “buy rating.” Thank you for reading, and I look forward to your comments below.

Read the full article here