Elevator Pitch

I rate CapitaLand Integrated Commercial Trust (OTCPK:CPAMF) [C38U:SP] as a Buy. I previously wrote about CPAMF’s value creation levers in my July 9, 2021 update for this commercial REIT.

With this latest write-up, I evaluate CapitaLand Integrated Commercial Trust’s recently disclosed financial performance for the second half of the prior year, and the REIT’s outlook for the intermediate term.

CPAMF’s 2H 2023 gross revenue and DPU (Distribution Per Unit) growth were reasonably good, and it has a favorable FY 2024-2026 outlook. There is justification for CapitaLand Integrated Commercial Trust trading at a lower yield (higher valuation) considering its DPU growth prospects, which explains why I have decided to stick with a Buy rating for the REIT.

Readers can trade in CapitaLand Integrated Commercial Trust shares on the Over-The-Counter market and the Singapore market. The trading liquidity of the REIT’s OTC shares with the CPAMF ticker symbol is low, considering its mean daily trading value of approximately $10,000 (source: S&P Capital IQ) for the past three months. Investors can consider dealing in CapitaLand Integrated Commercial Trust’s shares traded on the Singapore Stock Exchange, which boast a much higher three-month average daily trading value of $30 million as per S&P Capital IQ data. The REIT’s Singapore-listed shares with the C38U:SP ticker symbol can be bought or sold with US brokerages such as Interactive Brokers.

Recent 2H 2023 Results Were Decent

Last week, CapitaLand Integrated Commercial Trust revealed its 2H 2023 financial performance with an announcement issued on February 6. Note that the Singapore-listed REIT only reports its full financial results on a semi-annual basis.

CPAMF’s distribution per unit rose by +2.8% HoH (Half-on-Half) and +1.7% YoY to S$0.0545 in the second half of the previous year, as the REIT’s assets across different property segments performed well. Gross revenue for CapitaLand Integrated Commercial Trust’s office assets, integrated developments (assets with a mix of property types), and retail assets expanded by +6.5%, +4.3%, and +1.9%, respectively on a YoY basis for 2H 2023.

The REIT’s office properties witnessed a robust +9.0% rent reversion last year. CapitaLand Integrated Commercial Trust also disclosed in its 2H 2023 results presentation slides that the mean monthly rent per square foot for its Singapore office assets increased from S$10.41 as of June 30, 2023, to S$10.49 at the end of last year. These numbers imply that new leases with higher rental rates for its office properties have driven a +6.5% increase in the REIT’s 2H 2023 gross revenue for its office assets.

With respect to integrated developments, CapitaLand’s Raffles City Singapore asset was the star, as its overall (office and retail) occupancy rate increased from 95.3% at the end of 2022 to 98.7% as of December 31, 2023. During the same time period, the occupancy rate of Raffles City Singapore property’s retail component rose from 91.0% to 97.4%. The completion of the Asset Enhancement Initiatives or AEIs at Raffles City Singapore, as indicated in the chart presented below, was the major contributor to +4.3% YoY gross revenue growth for the REIT’s integrated developments in 2H 2023.

An Overview Of Asset Enhancement Initiatives At Raffles City Singapore Which Were Completed In 2022

CPAMF’s FY 2022 Results Presentation Slides

CapitaLand’s retail assets delivered an impressive rent reversion of +8.5% for 2023. In particular, it is worth paying attention to the relative outperformance of downtown retail properties over suburban retail properties. In the previous year, tenant sales and shopper traffic for CPAMF’s downtown retail assets grew by +2.5% YoY and +9.5% YoY, respectively. As a comparison, tenant sales and shopper traffic for the REIT’s suburban retail assets increased by +1.9% and +7.8%, respectively in YoY terms for 2023. At its FY 2023 results briefing, CPAMF highlighted on its latest earnings call that its downtown retail properties are benefiting from Singapore’s “push to increase the commercial activity outside of the core CBD (Central Business District).”

My view is that the REIT’s strong performance is sustainable. In the subsequent section, I detail the intermediate term prospects for CPAMF.

Mid-Term Outlook For CPAMF Is Positive

The sell side expects CapitaLand Integrated Commercial Trust’s distribution per unit or DPU in Singapore dollar terms to expand by +1.5% in FY 2024, before accelerating to +2.6% and +7.2% for FY 2025 and FY 2026, respectively as per S&P Capital IQ data. This translates into a pretty healthy DPU CAGR of +3.8% for CPAMF in the next three years. In contrast, the REIT’s FY 2017-2019 DPU CAGR prior to the COVID-19 outbreak was lower at +2.5%.

In my opinion, the market’s expectations of a faster rate of DPU growth for CapitaLand in the FY 2024-2026 time frame are reasonable.

Firstly, the REIT is anticipating a “mid-single” digit percentage rent reversion for its office assets and a rent reversion that is “not too far” from its +8.5% reversion last year for its retail properties this year, as per its comments at the recent FY 2023 results call.

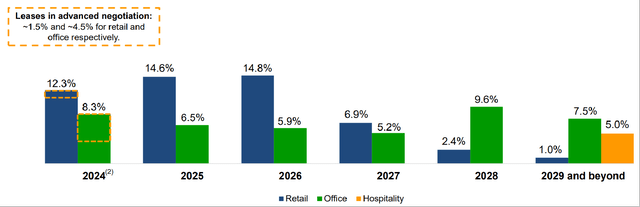

The Proportion Of CPAMF’s Leases That Expire Each Year By Property Type

CPAMF’s FY 2023 Results Presentation Slides

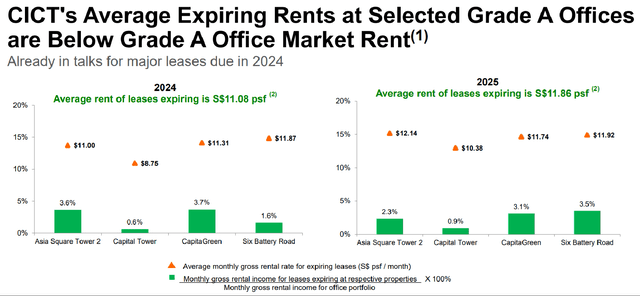

CapitaLand Integrated Commercial Trust noted at its FY 2023 analyst call that the outlook for its retail assets is favorable due to “limited availability of prime spaces in Singapore” and “very good demand from retailers.” At its most recent analyst briefing, CPAMF also mentioned that its office properties are likely to benefit from specific industries’ strong demand such as “the wealth and asset management, financial services, legal”, and “the flight to quality.” On the point about “quality”, it is worth noting that the rental rates for some of the REIT’s key grade A office asset leases due for expiry are lower than market rates as outlined in the chart presented below.

A Comparison Of The Expiring Rents And Market Rents For Certain Of CPAMF’s Office Assets

CPAMF’s FY 2023 Results Presentation Slides

In a nutshell, it is highly probable that CapitaLand Integrated Commercial Trust’s asset portfolio will continue to witness positive rent reversions for the foreseeable future.

Secondly, CPAMF’s future DPU growth is expected to be supported by new AEIs or Asset Enhancement Initiatives.

In the preceding section, I have already indicated how the AEI at the Raffles City Singapore property drove 2H 2023 gross revenue growth of +4.3% YoY for the REIT. CPAMF described AEIs as “planting the flag along the runway to allow a more sustainable kind of income growth” at its latest analyst call. Looking ahead, CapitaLand Integrated Commercial Trust revealed in its FY 2023 results presentation that it has plans to execute AEIs at three assets, namely “IMM Building, Gallileo and 101 Miller Street.”

Thirdly, there are opportunities for CapitaLand to sell certain assets and subsequently re-allocate the asset sales proceeds to new higher-returning properties.

The deal-making environment seems to have gotten better judging by CPAMF’s recent comments, which increases the probability of property divestitures materializing in the near term. At the REIT’s FY 2023 results call, CapitaLand emphasized that “there has been interest (in the acquisition of office and retail assets) returning”, which is a “reflection of better risk appetite.” According to a February 8, 2024 news article published in Singapore media The Business Times, the REIT’s “Bukit Panjang Plaza and 21 Collyer Quay” properties are speculated to be the assets that CPAMF could possibly be considering for disposal.

Lastly, the REIT might see its finance costs decrease going forward, assuming that it is successful with its deleveraging efforts.

CapitaLand Integrated Commercial Trust’s interest expense rose by +21.8% YoY to S$168 million in the second half of 2023. In other words, the REIT would have recorded much stronger DPU growth for 2H 2023, if it had lower financial leverage. CPAMF’s goal is to reduce its financial leverage (debt-to-assets) metric from 39.9% as of end-2023 to between 37% and 38% (source: FY 2023 analyst briefing commentary) in time to come. As such, it will be reasonable to expect a decrease in finance costs to boost the REIT’s DPU in the future.

Final Thoughts

I continue to award a Buy rating to CapitaLand Integrated Commercial Trust. The market currently values the REIT at a consensus next twelve months’ distribution or dividend yield of 5.51% (source: S&P Capital IQ), which is above its historical 15-year average distribution yield of 5.36%. In the past 15 years, CPAMF has traded at a dividend yield of as low as 3.03%.

I am of the view that the REIT can trade at a more demanding valuation or a lower distribution yield in the 4.5%-5.0% range. This takes into account my expectations that its DPU growth will accelerate from +2.5% for FY 2017-2019 (pre-pandemic years) to +3.8% in the FY 2024-2026 time period.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here