Should you hold cash or invest in the market? Attractive yields on savings and cash-like investments can make it tempting to hold cash instead of investing extra money. On the heels of the worst year ever for bonds and the seventh worst year for stocks, the hesitation is understandable.

But before proclaiming cash is king and parking your money in an FDIC insured bank account, consider your time frame and how you plan to use the money. If the funds aren’t earmarked for anything in the near term, holding cash could be short-sighted.

Hold cash or invest?

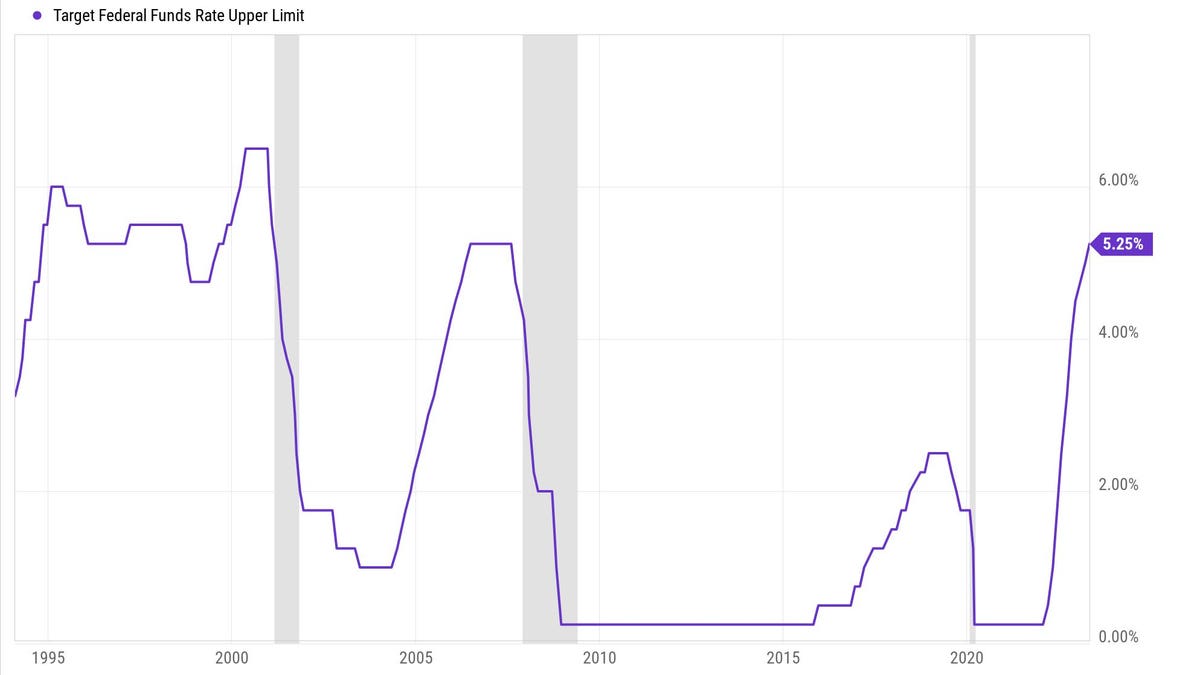

Interest rates have skyrocketed since the end of 2021. In fact, the Federal Reserve has raised the upper limit federal funds rate by 5% since the beginning of 2022. This has been the faster pace of rate hikes since the 1980-1981 cycle. The federal funds rate hasn’t been this high since 2007 when it peaked at 5.25%. The prior peak was 6.50% in the late 2000s. These rate hikes put stocks and bonds under pressure last year. The silver lining is cash (and equivalents), such as money markets, high-yield savings accounts, CDs, and short-term U.S. Treasuries, are now offering an attractive return.

But it won’t last forever. For those considering holding cash instead of investing, recognize that this strategy has risks too.

Reinvestment risk

For investors holding cash, reinvestment risk should be of concern. Reinvestment risk happens when rates decline and maturing cash flows or variable rate accounts are reinvested at a lower interest rate. Before discussing reinvestment risk in detail, it’s important to understand a few key points about yield curves.

Understanding the yield curve

When interest rates change, they don’t often do so uniformly across the curve. The current rate hike cycle illustrates this quite well, given the speed. The federal funds rate is the shortest of short-term interest rates. It’s the reference interest rate for overnight borrowing between financial institutions like banks. So when the federal funds rate goes up, it can have an outsized impact on shorter term interest rates on assets like Treasury bills (T-bills).

Longer term rates, such as a five or 10-year Treasury, also move in response to a changing federal funds rate, but these yields are driven more by what market participants expect the average yield to be over this period, which is also influenced by inflation and economic growth expectations. Markets recognize that the Federal Reserve cannot hold interest rates at the current level for the next decade, so future cuts are priced in.

In the chart above, it’s worth noting that the 1-month T-bill rate is being distorted by the debt ceiling talks.

Comparing yields

To help investors compare cash and equivalents, interest rates (or yields) are usually in annualized terms. For example, the annual percentage yield (APY

PY

Compare that to the stated yield of 5.6% on a 1-month T-bill, which is roughly .467% a month. Again just using simple math, this presumes the par value will roll over each month and reinvest at the same rate to get to the annual yield.

A 1-year Treasury currently yields about 4.9%. This is what the market currently expects interest rates to average over the next year. It’s lower than the 1-month T-bill because market participants generally expect rates to decline during this time. And the 1-month bill is spiking because of the debt ceiling. But if we do see rate cuts, an investor would not be able to roll their 1-month bill over at .467% for the next 12 months, it would be something less.

So while the savings account or T-bill might look more attractive than a 1-year Treasury initially, remember, only the 1-year Treasury yield is locked in (if held to maturity). If/when interest rates drop, interest rates in savings accounts will fall too, along with 1-month bills.

This is reinvestment risk.

If the investor can no longer reinvest a 1-month bill at the same rate, there will eventually be a crossover point when locking in a lower stated yield would be better on comparison. Investors parking cash on the short end of the curve should be aware of this. As illustrated in the chart below, short-term rates (in T-bills, savings accounts, money markets, etc.) generally track very closely to the federal funds rate.

Cash isn’t an investment strategy

For individuals with upcoming cash needs, perhaps for a renovation, taxes, or college, staying liquid in a high yield money market or locking in returns with a Treasury ladder can make a lot of sense. And finding ways to optimize necessary cash holdings is a prudent part of any financial plan. But holding cash isn’t a wealth-building strategy.

In fact, according to The Wall Street Journal, since 1928 cash only outperformed both stocks and bonds over a calendar year 12 times. Put another way, 87% of years cash wasn’t king!

To illustrate, this chart shows the growth of $1M invested in stocks (S&P 500) vs cash (Bloomberg 1-3 month US Treasury index) over 10 years.

Cash vs stocks: growth of $1M

With an average annualized return under 1%, the cash portfolio only gains $92,000 over a decade. If we go all the way back to May 1997 (and include the dot-com bust, Great Financial Crisis, and the Covid crash), stocks returned roughly 8.3% on average annually versus cash at 1.9%.

Of course, in bouts of market volatility over shorter periods of time, cash can certainly outperform stocks. Since the beginning of 2022, cash has outperformed the S&P 500 by about 14% on a cumulative total return basis. But again, if history is a guide, this relationship will reverse and we’ve already seen it to start the year.

Another point to keep in mind is that these examples all are reflected in nominal terms. Real (inflation-adjusted) returns for cash would be negative. This is a central reason that holding cash isn’t a way to build wealth or even preserve it over time.

Consider your objectives

Before making an asset allocation decision, always keep in mind what you’re trying to accomplish. Holding cash isn’t going to help build or preserve wealth over time. But if you’re setting money aside for an upcoming expense, you should absolutely try using the yield curve to your advantage to optimize cash returns.

If you’re trying to time the market out of concern for near term market moves, proceed with caution. Successfully doing so requires you to be right twice: when you get out and back in. History shows that the best days in the market tend to happen right around the worst ones. So before deciding to hold cash instead of investing, consider your goals.

Read the full article here